Student-t Distribution

Student’s t

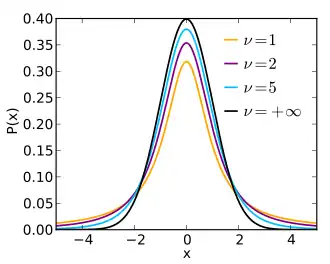

Probability density function

|

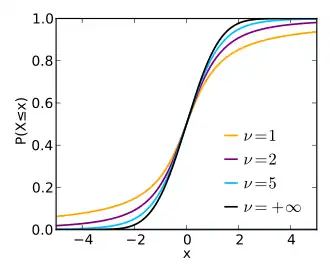

Cumulative distribution function

|

| Parameters

|

ν > 0 degrees of freedom (real)

|

| Support

|

x ∈ (−∞; +∞)

|

| PDF

|

|

| CDF

|

![{\displaystyle {\begin{matrix}{\frac {1}{2}}+x\Gamma \left({\frac {\nu +1}{2}}\right)\cdot \\[0.5em]{\frac {\,_{2}F_{1}\left({\frac {1}{2}},{\frac {\nu +1}{2}};{\frac {3}{2}};-{\frac {x^{2}}{\nu }}\right)}{{\sqrt {\pi \nu }}\,\Gamma \left({\frac {\nu }{2}}\right)}}\end{matrix}}}](../../_assets_/eb734a37dd21ce173a46342d1cc64c92/02732e546784af1fb16d0dc1bb65dd743e2284ad.svg)

where 2F1 is the hypergeometric function

|

| Mean

|

0 for ν > 1, otherwise undefined

|

| Median

|

0

|

| Mode

|

0

|

| Variance

|

for ν > 2, ∞ for 1 < ν ≤ 2, otherwise undefined for ν > 2, ∞ for 1 < ν ≤ 2, otherwise undefined

|

| Skewness

|

0 for ν > 3, otherwise undefined

|

| Ex. kurtosis

|

for ν > 4, ∞ for 2 < ν ≤ 4, otherwise undefined for ν > 4, ∞ for 2 < ν ≤ 4, otherwise undefined

|

| Entropy

|

...

|

| MGF

|

undefined

|

| CF

|

for ν > 0 for ν > 0

(x): Bessel function[1] (x): Bessel function[1]

|

Student t-distribution (or just t-distribution for short) is derived from the chi-square and normal distributions. We divide the standard normally distributed value of one variable over the root of a chi-square value over its r degrees of freedom. Mathematically, this appears as:

where  and

and  .

.

External links

- ↑ Hurst, Simon, The Characteristic Function of the Student-t Distribution, Financial Mathematics Research Report No. FMRR006-95, Statistics Research Report No. SRR044-95