For data that is known to have seasonal, or daily patterns I'd like to use fourier analysis be used to make predictions. After running fft on time series data, I obtain coefficients. How can I use these coefficients for prediction?

I believe FFT assumes all data it receives constitute one period, then, if I simply regenerate data using ifft, I am also regenerating the continuation of my function, so can I use these values for future values?

Simply put: I run fft for t=0,1,2,..10 then using ifft on coef, can I use regenerated time series for t=11,12,..20 ?

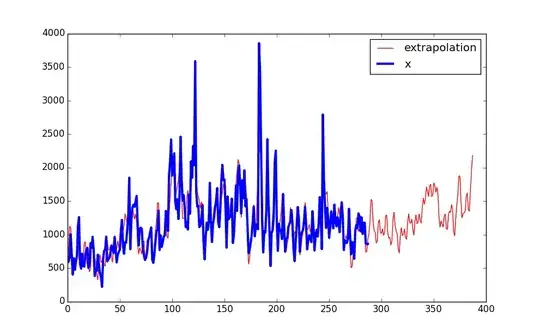

P.S. Locally Stationary Wavelet may be better than fourier extrapolation. LSW is commonly used in predicting time series. The main disadvantage of fourier extrapolation is that it just repeats your series with period N, where N - length of your time series.

P.S. Locally Stationary Wavelet may be better than fourier extrapolation. LSW is commonly used in predicting time series. The main disadvantage of fourier extrapolation is that it just repeats your series with period N, where N - length of your time series.